- Contractors

- Junior Professional

How to develop critical thinking skills in finance & accounting

Stephen Moir

Share this:.

- Click to share on Facebook (Opens in new window)

- Click to share on Twitter (Opens in new window)

- Click to share on LinkedIn (Opens in new window)

- Click to email a link to a friend (Opens in new window)

When it comes to finance and accounting roles, employers are increasingly looking for problem solvers, not a number-crunchers. Over recent years, we have seen an increasing demand for people who can analyse and interpret data and think critically.

What is critical thinking.

A critical thinker is a problem solver. They are able to evaluate complex situations, weigh-up different options and reach logical (and often quite creative) conclusions.

Critical thinkers are highly-valued by employers as they innovate and make improvements, without taking unnecessary risks. Chartered Accountants Australia and New Zealand recently identified that it was in the top 10 attributes that will help you get noticed in the job market.

Why are critical thinking skills important?

Once you have learnt how to develop critical thinking skills you will be better able to add value to data, interpret trends within the business, understand how people and performance intersect and take-on broader commercial outlook that benefits the business.

How to develop critical thinking skills

Critical thinking comes naturally to some people, but it is also a skill than can be practiced. Here are some tips for how to develop your own critical thinking skills :

- Examine: Self-awareness is the foundation of critical thinking. It allows you to play to your strengths and address your weaknesses. Question how and why you do things the way you do.

- Analyse: Look for opportunities to grow and improve. Consider alternative solutions to the problems you encounter in your work.

- Explain: Clear communication is key. Get into the habit of talking through your reasoning and conclusions with colleagues.

- Innovate: Develop an independent mind-set. Find ways to think outside the box and challenge the status quo. Make sure your decisions are well-thought out. A critical thinker is logical as well as creative.

- Learn: Keep an open and well-oiled mind. Brush-up on your problem-solving skills by doing brain-teasers or trying to solve problems backwards. Keep up-to-date with professional learning opportunities . You may also need to unlearn past mindsets in order to grow and move forward.

How to apply critical thinking skills in your current role

Could you implement a new process or procedure that enhances performance or profitability? You might also consider volunteering for a new project or responsibility that gives you the opportunity to innovate and take on a new challenge. It’s a great way to broaden your skillset and gain exposure to other parts of the business.

Surround yourself with other critical thinkers in the organisation and work together towards achieving a problem-solving culture. Ask questions, and always look for opportunities for continual learning.

Changing roles to develop critical thinking skills

At Moir Group, we are passionate about finding the right cultural fit between people and the organisations they work with. If you are a critical thinker, it’s worth looking for a stimulating work environment that encourages innovation and non-conformist thinking when considering your next role.

How to demonstrate critical thinking skills at an interview

During an interview, use examples from your past experiences to demonstrate your problem-solving abilities. Show that you can be analytical, weigh-up pros and cons, consider other view points and be creative in your solutions. Clearly articulating your thought process is key.

Sometimes an interviewer will ask you to simplify the complex as a way of determining your clarity of thought. For example: “How would you explain the state of the economy to a kindergarten child?” In instances like these, the focus will be on how you explain your reasoning, rather than achieving a ‘right’ answer. Learn more here.

If you’re looking to take that next step in your career, we can help. Get in touch with us here .

2 Responses to “How to develop critical thinking skills in finance & accounting”

Hi Stephen,

The above is very useful and very valuable for employers. However my understanding of critical thinking is slightly different from above. I recently listened to a course in critical thinking by Professor Steven Novella of Yale School of Medicine. To keep it simple it is to do with assessing the veracity of views and statements made by oneself, others and media being constantly aware of the many biases, the flaws and fabrications of memory, half truths, unspoken truths, and even lies. So it becomes key to adopt an inquisitive mindset, to look for external evidence that supports argument and not just wishful or hopeful thinking.

Just wanting to add to the debate as this is a really important area.

Hi Richard,

We are pleased that found this article useful. Thanks for your sharing your thoughts about critical thinking.

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

Moir Group acknowledges Traditional Owners of Country throughout Australia and recognises the continuing connection to lands, waters and communities. We pay our respect to Aboriginal and Torres Strait Islander cultures; and to Elders past and present and encourage applications from Aboriginal and Torres Strait Islander people and people of all cultures, abilities, sex, and genders.

- Kreyòl Ayisyen

Financial knowledge and decision-making skills

Financial knowledge and decision-making skills help people make informed financial decisions through problem-solving, critical thinking, and an understanding of key financial facts and concepts.

Building financial knowledge and decision-making skills

How do we learn to make good financial choices? Learn more about the financial knowledge and decision-making skills building block and how it can help young people make the right decisions for their situation.

Importance of financial knowledge and decision-making skills

Strong financial knowledge and decision-making skills help people weigh options and make informed choices for their financial situations, such as deciding how and when to save and spend, comparing costs before a big purchase, and planning for retirement or other long-term savings.

Development of this building block

Financial knowledge and decision-making skills typically don’t develop until adolescence and young adulthood. During these years, they become more relevant, especially for youth who start to earn money, buy things on their own, manage a bank account, or borrow for education.

The tables that follow show what this building block looks like at three stages of development and how the skills and abilities relate to adult behavior associated with financial well-being.

Early childhood (ages 3–5)

| Milestones for financial knowledge and decision-making skills | What it may look like in adulthood |

|---|---|

Has early math skills like counting and sorting | Calculates change owed at point of sale, categorizes spending for budgeting, tracks cash flow |

Grasps very basic financial concepts like money and trading | Estimates costs, calculates discounts or sales tax |

Middle childhood (ages 6–12)

| Milestones for financial knowledge and decision-making skills | What it may look like in adulthood |

|---|---|

Understands basic financial concepts | Has a realistic idea of how much things cost, saves a portion of earnings, pays bills on time, makes a budget |

Successfully manages money (like their allowance) or other resources to reach personal goals | Spends to meet needs before wants, follows a budget, saves for big purchases or events (e.g., vacation) |

Adolescence and early adulthood (ages 13–21)

| Milestones for financial knowledge and decision-making skills | What it may look like in adulthood |

|---|---|

Understands advanced financial concepts and processes | Understands risks and benefits of investing, uses credit wisely, manages debt |

Routinely manages money or other resources to reach personal goals | Spends with values and goals for today and the future in mind, pays day-to-day and month-to-month expenses, saves for retirement, has financial flexibility to splurge once in a while |

Identifies trusted sources of financial information and accurately uses them to compare and make decisions | Seeks credible information (e.g., “Consumer Reports,” product labels, store ads), compares features and costs before making big purchases, consults trusted advisers, knows the difference between a bargain and a scam |

Teaching this building block

Schools can provide opportunities for youth to practice financial behaviors, make financial decisions, and reflect on the outcomes and consequences of those decisions. Across the curriculum, teachers can provide opportunities for students to learn how to find and recognize reliable financial information, compare financial products, and do purposeful financial research in order to analyze options and make decisions.

Instructional strategies

Research shows that the following strategies can be effective to help people develop financial knowledge and decision-making skills.

- Competency-based learning: Student-centered learning that encourages students to progress toward well-defined benchmarks to give them a sense of mastery and ownership over the skills and knowledge they are learning

- Direct instruction: A structured, straightforward, teacher-directed approach that focuses on an explicit skill and typically includes a lecture, demonstration, or discussion

- Personalized instruction: Teacher assesses each student’s needs, then tailors instruction to the individual student, including focusing and differentiating resources, strategies, supports, and pacing on that student’s needs to individualize learning

- Project-based learning: A hands-on strategy in which students actively explore real-world challenges, answer meaningful questions, and accomplish relevant tasks and, in doing so, are encouraged to make their own decisions, perform their own research, overcome obstacles, and present their work to others

- Simulation: Hands-on learning activities that use real-world scenarios to promote critical thinking and application of learning

Learning activities

Learning activities that nurture financial knowledge and decision making should support young people’s acquisition of factual knowledge, research and analysis skills, and deliberate financial decision-making. The types of activities that support these skills include the following.

- Financial coaching and mentoring: Adults engage and encourage students (individually and in small groups) to develop financial capability and work toward financial goals

- Financial simulations: Educational tools or activities that replicate real-world financial management situations and allow students to develop skills such as budgeting, comparison shopping, and investing by making mock decisions that result in realistic consequences

- Real-world case studies: Stories that present realistic situations involving a dilemma, conflict, or problem to be negotiated or resolved by analyzing and evaluating a range of information and weighing the consequences of different decisions

Resources for teaching financial knowledge and decision-making skills

- Search for classroom activities to nurture the development of financial knowledge and decision-making skills

- Explore all strategies and learning activities for nurturing the building blocks

This site uses cookies, including third-party cookies, to improve your experience and deliver personalized content.

By continuing to use this website, you agree to our use of all cookies. For more information visit IMA's Cookie Policy .

Change username?

Create a new account, forgot password, sign in to myima.

Multiple Categories

Improving Critical Thinking Skills

November 01, 2021

By: Sonja Pippin , Ph.D., CPA ; Brett Rixom , Ph.D., CPA ; Jeffrey Wong , Ph.D., CPA

Whether working with financial statements, analyzing operational and nonfinancial information, implementing machine learning and AI processes, or carrying out many of their other varied responsibilities, accounting and finance professionals need to apply critical thinking skills to interpret the story behind the numbers.

Critical thinking is needed to evaluate complex situations and arrive at logical, sometimes creative, answers to questions. Informed judgments incorporating the ever-increasing amount of data available are essential for decision making and strategic planning.

Thus, creatively thinking about problems is a core competency for accounting and finance professionals—and one that can be enhanced through effective training. One such approach is through metacognition. Training that employs a combination of both creative problem solving (divergent thinking) and convergence on a single solution (convergent thinking) can lead financial professionals to create and choose the best interpretations for phenomena observed and how to best utilize the information going forward. Employees at any level in the organization, from newly hired staff to those in the executive ranks, can use metacognition to improve their critical assessment of results when analyzing data.

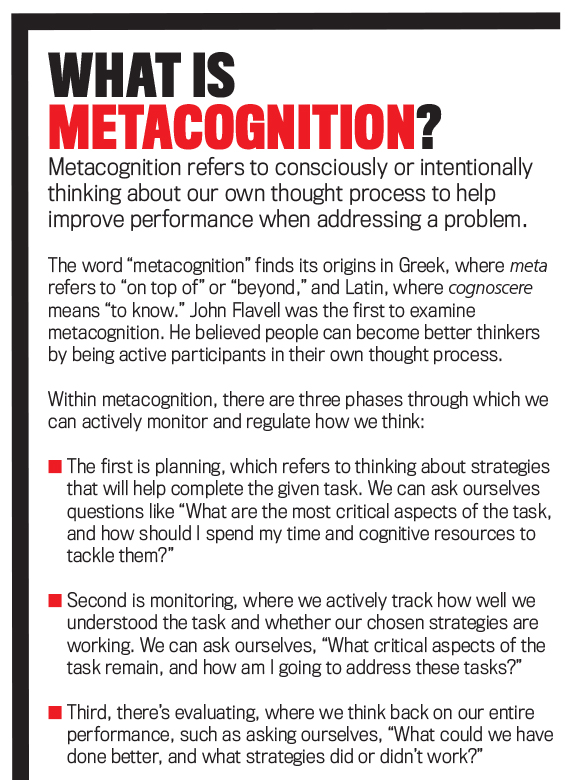

THINKING ABOUT THINKING

Metacognition refers to individuals’ ability to be aware, understand, and purposefully guide how to think about a problem (see “What Is Metacognition?”). It’s also been described as “thinking about thinking” or “knowing about knowing” and can lead to a more careful and focused analysis of information. Metacognition can be thought about broadly as a way to improve critical thinking and problem solving.

In their article “Training Auditors to Perform Analytical Procedures Using Metacognitive Skills,” R. David Plumlee, Brett Rixom, and Andrew Rosman evaluated how different types of thinking can be applied to a variety of problems, such as the results of analytical procedures, and how those types of thinking can help auditors arrive at the correct explanation for unexpected results that were found ( The Accounting Review , January 2015). The training methods they describe in their study, based on the psychological research examining metacognition, focus on applying divergent and convergent thinking.

While they employed settings most commonly encountered by staff in an audit firm, their approach didn’t focus on methods used solely by public accountants. Therefore, the results can be generalized to professionals who work with all types of financial and nonfinancial data. It’s particularly helpful for those conducting data analysis.

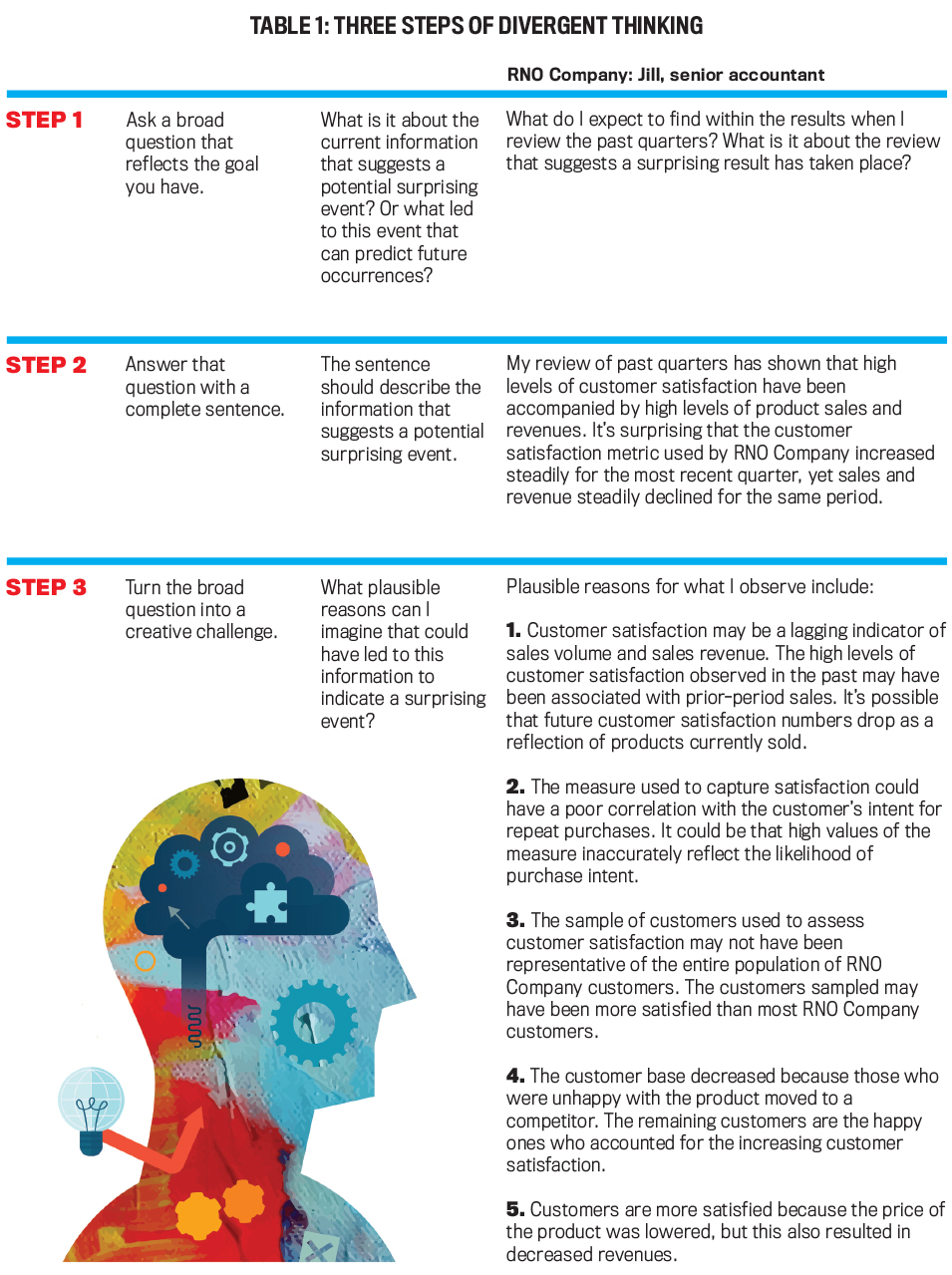

Their approach involved a sequential process of divergent thinking followed by convergent thinking. Divergent thinking refers to creating multiple reasons about what could be causing the surprising or unusual patterns encountered when analyzing data before a definitive rationale is used to inform what actions to take or strategy to use. Here’s an example of divergent thinking:

The customer satisfaction metric employed by RNO Company has increased steadily for the quarter, yet its sales numbers and revenue have declined steadily for the same period. Jill, a senior accountant, conducted ratio and trend analyses and found some of the results to be unusual. To apply divergent thinking, Jill would think of multiple potential reasons for this surprising result before removing any reason from consideration.

Convergent thinking is the process of finding the best explanation for the surprising results so that potential actions can be explored accordingly. The process consists of narrowing down the different reasons by ensuring the only reasons that are kept for consideration are ones that explain all of the surprising patterns seen in the results without explaining more than what is needed. In this way, actions can be taken to address the heart of any problems found instead of just the symptoms. On the other hand, if the surprising result is beneficial to an organization, it can make it easier to take the correct actions to replicate the benefit in other aspects of the business. Here’s an example of convergent thinking:

Washoe, Inc.’s customer satisfaction metric has increased steadily for the quarter, yet sales numbers and revenue have steadily declined for the same period. Roberto found this result to be surprising. After employing divergent thinking to identify 10 potential reasons for this result, such as “the reason that customers seem more satisfied is that the price of goods has been reduced, which also explains the reduction in sales revenue.” To apply convergent thinking, Roberto reviewed each reason that best fit. If the reason doesn’t explain the unusual results satisfactorily, then it will either be modified or discarded. For example, the reduced price of goods doesn’t explain all of the results—specifically, the decrease in units sold—so it needs to either be eliminated as a possible explanation or modified until it does explain all the results.

Exploring strategic or corrective actions based on reasons that completely explain the unusual results increases the chance of correctly addressing the actual issue behind the surprising result. Also, by making sure that the reason doesn’t contain extraneous details, unneeded actions can be avoided.

It’s important to note that a sequential process is required for these types of thinking to be most effective. When encountering a surprising or unexpected result during data analysis, accounting professionals must first focus strictly on divergent thinking—thinking about potential reasons—before using convergent thinking to choose a reason that best explains the surprising result. If convergent thinking is used before divergent thinking is completed, it can lead to reasons being picked simply because they came to mind right away.

LEARNING THE PROCESS

Improving divergent and convergent thinking can benefit employees at any level of an organization. Newer professionals who don’t have as much technical knowledge and experience to draw upon may be more likely to focus on the first explanation that comes to mind (“premature convergent thinking”) without fully considering all of the potential reasons for the surprising results. Experienced individuals such as CFOs and controllers have more technical knowledge and practical experience to rely on, but it’s possible these seasoned employees fall into habits and follow past patterns of thought without fully exploring potential causes for surprising results.

Instructing all accounting professionals on how to think about surprising results can help them have a more complete understanding of the issues at hand that will help guide actions taken in the future. It can lead to a more creative approach when analyzing information and ultimately to better problem solving.

When teaching employees to use divergent and convergent thinking, the goal is to get them to focus on what should be done once they identify information that suggests a surprising result has occurred. The first step is to learn how to properly use divergent thinking to create a set of plausible explanations more likely to contain the actual reason for the surprising results. There’s a three-step method that individuals can follow (see Table 1):

- Ask a broad question that reflects the goal you have: For instance, what is it about the current information that suggests a potential surprising event? Or what led to this event that can help predict future occurrences?

- Answer that question with a complete sentence: Be sure the answer includes a description of the information that suggests a potential surprising event.

- Turn the broad question into a creative challenge: Identify the plausible reasons that could have led to the indications of a surprising event.

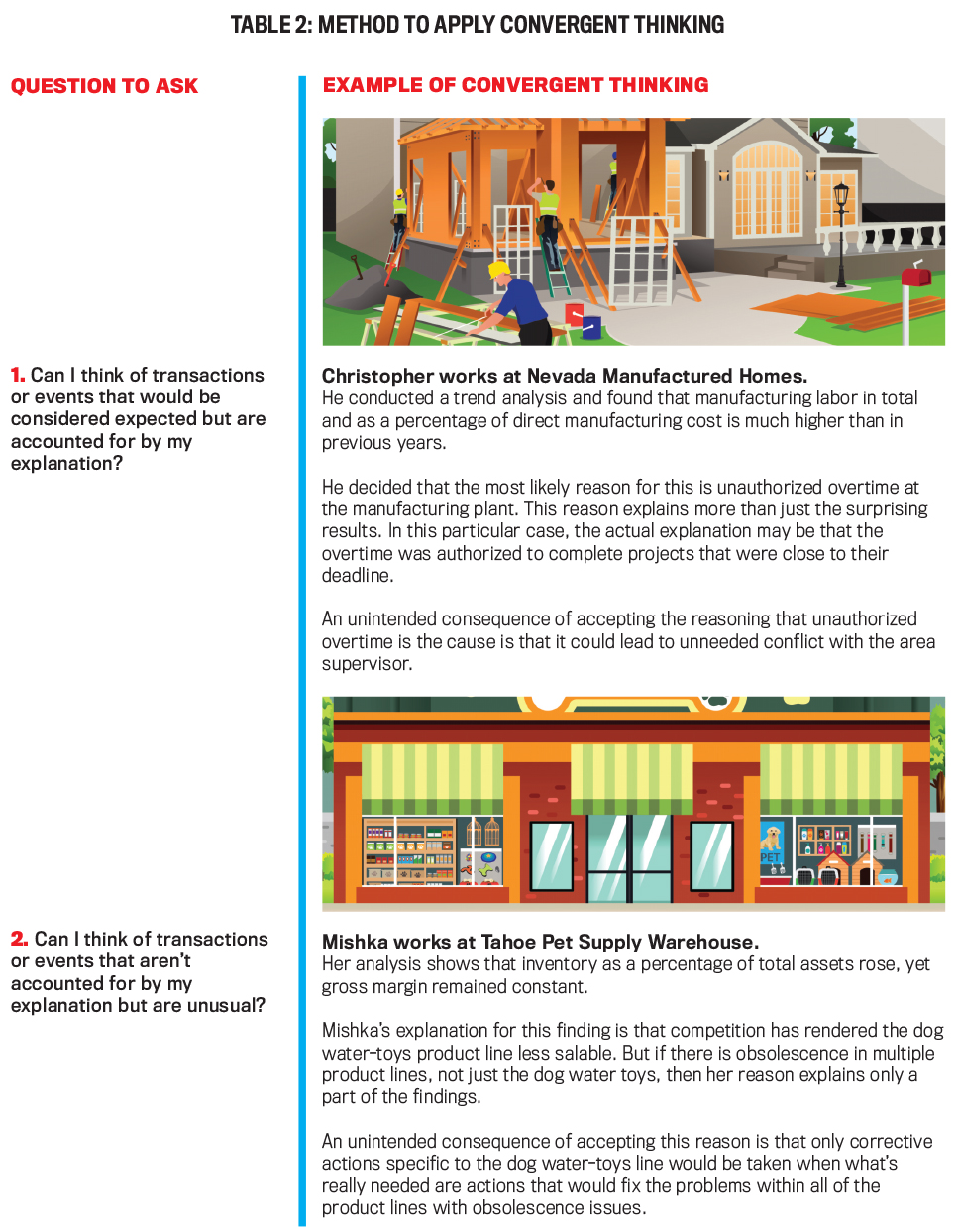

Once employees have a good grasp of how to use divergent thinking, the next step is to instruct them in the proper use of convergent thinking, which involves choosing the best possible reason from the ones identified during the divergent thinking process. Potential reasons need to be narrowed down by removing or modifying those that either don’t fully explain the surprising results or that overexplain the results.

Two simple questions can help individuals screen each of the possible explanations generated in the divergent thinking process (see Table 2):

- Can I think of transactions or events that would be considered expected but are accounted for by my explanation?

- Can I think of transactions or events that aren’t accounted for by my explanation but are unusual?

The first question is designed for an individual to think about whether there are other events outside of the current issue that fit the explanation: “Does the explanation also address phenomena that aren’t related to or outside the scope of the surprising result that’s being studied?” If the answer is “yes,” then this is a case of overexplanation. Consider, for example, a scenario involving an increase in bad debts. Relaxing credit requirements may explain the increase, but they would also explain a growth in sales and falling employee morale due to working massive amounts of overtime to make products for sale.

The second question is designed to think about whether an explanation only accounts for part of the phenomenon being observed: “Does the explanation address only part of what’s being observed while leaving other important details unexplained?” If the answer is “yes,” then it’s an under-explanation. For example, consider a decline in sales. An economic downturn at the same time as the decline may be a possible explanation, but it might only be part of the problem. A drop in product quality or a drop in demand due to obsolescence could also be causing sales to decline.

If the answer to either screening question is “yes,” then the explanation needs to be discarded from consideration or modified to better address the concern. In the case of over-explanation, the reason is too general and may lead to action areas where none is needed while still not addressing the actual issue. For underexplanation, the reason is incomplete because it accounts for only a portion of the phenomenon observed, thus action may only address a symptom and not the actual root problem.

If the answer to both questions is “no,” then the explanation is viable. The chosen reason neither overexplains nor underexplains the issue at hand, making it more likely that the recommended solution or plan of action based on that reason will be more successful at addressing the actual cause of the issue.

Divergent and convergent thinking are two distinct processes that work in conjunction with each other to arrive at potential reasons for the results they observe. Yet, as previously noted, the two ways of thinking must be conducted separately and sequentially in order to obtain optimal results. Divergent thinking must be applied first in order to achieve a diverse set of potential reasons. This will maximize the probability of generating a feasible reason that explains the results correctly. After the set of potential reasons has been generated using the divergent thinking approach, convergent thinking should be used to methodically remove or modify the reasons that don’t fit with the surprising results.

If both divergent thinking and convergent thinking are done simultaneously, premature convergence can lead to a less-than-optimal reason being chosen, which may lead to taking the wrong course of action. Thus, it’s important with training to instruct employees in the use of both divergent thinking and convergent thinking and to use the types of thinking sequentially.

ORGANIZATIONAL TRAINING

Learning to apply divergent and convergent thinking can require a substantial time commitment. The process we’ve described here is designed to enhance critical thinking and problem-solving skills. It outlines a general approach that doesn’t provide specific guidance on the best methods to analyze data or complete a task but rather focuses on successful methods to think of a diverse set of reasons for any surprising results and then how to choose the best explanation for that result in order to be able to recommend the most appropriate actions or solutions.

Individuals can practice the approach we’ve described on their own, but each organization will likely have its own preferred way to approach the analyses. Plumlee, et al., used training modules in their study that could be employed in a concerted effort by a company, with supervisors training their employees. We estimate that a basic training session would take about two hours. Complete training with practice and feedback would require about four hours—which could grow longer with even more for intensive training.

One area where this training could be very effective in helping employees is data analytics. In the past decade, an increasing amount of accounting and financial work involves or relies on data analysis. Data availability has increased exponentially, and companies use or have developed software that generates sophisticated analytical results.

Typical data analysis procedures accounting professionals might be called on to perform include things such as ratio and trend analyses, which compare financial and nonfinancial data over time and against industry information to examine whether results achieved are in line with expectations for strategic actions. Additionally, analyses are forward-looking when performance measures examined are leading indicators.

In order to perform data analytics effectively, accounting professionals must exercise sufficient judgment to critically assess the implications of any surprising results that are found. The quality of judgments and understanding the best ways to conduct and interpret the information uncovered by data analytics have typically been a function of time spent on the job along with training. At the same time, however, it’s commonplace that many of these analyses are performed by newer professionals.

Training in metacognition will help these employees more effectively and creatively reach conclusions about what they’ve observed in their analysis. Since the method discussed provides general instruction, each organization can customize the approach to best fit its own operations, strategies, and goals. Implementing a training program can be worth the investment given the importance of critical thinking throughout the process of evaluating operating results. Avoiding potential failures with interpreting results that could be prevented would seem to warrant the consideration of metacognitive training.

About the Authors

November 2021

- Strategy, Planning & Performance

- Business Acumen & Operations

- Decision Analysis

- Operational Knowledge

Publication Highlights

Lessons from an Agile Product Owner

Explore more.

Copyright Footer Message

Lorem ipsum dolor sit amet

.png "critical thinking in financial")

- Get started

How to Improve Your Critical Thinking Skills as a VP of Finance

Master critical thinking as a finance VP. Strengthen decision making, risk management & strategy formulation with these expert tips.

As the VP of Finance for your organization, you have a crucial role to play in driving growth and ensuring financial stability. To achieve these goals, it is essential to possess strong critical thinking skills that can help you make sound financial decisions and navigate complex financial landscapes. In this article, we will explore how you can improve your critical thinking skills and become a more effective leader in the world of finance.

Understanding the Importance of Critical Thinking in Finance

Critical thinking is an essential skill for anyone working in finance. It involves the ability to analyze information objectively, evaluate different perspectives, and make informed decisions. As a VP of Finance, you are responsible for monitoring financial performance, identifying risks, and ensuring that financial goals are met. To achieve these objectives, you need to be able to think critically about financial information and make sound financial decisions.

The role of critical thinking in financial decision-making

When it comes to financial decision-making, critical thinking can make all the difference. It helps you evaluate different options and assess their potential impacts on your organization. By considering various scenarios and weighing the pros and cons of different decisions, you can make informed choices that promote financial success.

For example, let's say you're considering investing in a new product line. Critical thinking would require you to analyze the potential market demand for the product, the costs associated with production and marketing, and the potential revenue it could generate. By weighing these factors, you can make an informed decision about whether or not to invest in the product line.

How critical thinking skills can enhance your financial strategies

Critical thinking skills can also help you develop more effective financial strategies. By analyzing financial data, identifying trends, and anticipating potential risks, you can develop strategies that take advantage of financial opportunities while mitigating potential risks. This can help your organization achieve long-term financial stability and growth.

For instance, let's say you're developing a budget for the upcoming fiscal year. Critical thinking skills would require you to analyze past financial data, identify potential areas of cost savings, and anticipate any potential financial risks. By doing so, you can develop a budget that is realistic, achievable, and aligned with your organization's financial goals.

In conclusion, critical thinking is a crucial skill for anyone working in finance. By developing your critical thinking skills, you can make informed financial decisions, evaluate different options, and develop effective financial strategies that promote long-term financial success.

Assessing Your Current Critical Thinking Abilities

Before you can improve your critical thinking skills, it's important to assess where you stand. By identifying your strengths and weaknesses, you can develop a roadmap for improvement that is tailored to your individual needs.

One way to assess your critical thinking abilities is to evaluate your problem-solving skills. Are you able to identify the root cause of a problem and develop effective solutions? Do you consider all possible options before making a decision?

Another important aspect of critical thinking is the ability to analyze information and make informed judgments. Are you able to identify relevant information and separate it from irrelevant data? Do you consider the reliability and credibility of your sources?

Identifying your strengths and weaknesses

Start by taking a close look at your critical thinking abilities. Identify areas where you excel, such as analyzing financial data or assessing risks. On the other hand, identify areas where you may need improvement, such as evaluating different perspectives or identifying biases.

It's important to remember that everyone has strengths and weaknesses when it comes to critical thinking. By identifying your areas of weakness, you can focus on improving those skills and becoming a more well-rounded critical thinker.

Seeking feedback from colleagues and mentors

It's also important to seek feedback from colleagues and mentors. By getting an outside perspective, you can gain valuable insights into your strengths and weaknesses and identify areas for improvement. Be open to constructive criticism and use it as an opportunity to grow and develop as a leader.

Additionally, seeking feedback from a diverse group of individuals can help you identify blind spots and biases that you may not have been aware of. This can help you become a more objective and effective critical thinker.

Remember, critical thinking is a skill that can be developed and improved over time. By assessing your current abilities, identifying areas for improvement, and seeking feedback from others, you can become a more effective and successful leader.

Developing a Growth Mindset for Continuous Improvement

Improving your critical thinking skills requires a growth mindset, where you are open to learning, growth, and development. Embrace challenges and view them as opportunities to learn and develop your skills.

One way to embrace challenges is to set goals for yourself. Whether it's a personal or professional goal, having a clear objective in mind can help motivate you to push yourself beyond your comfort zone. Additionally, breaking down your goals into smaller, achievable steps can make them feel less daunting and more manageable.

Embracing challenges and learning from failures

Don't be afraid to take on new challenges and stretch yourself beyond your comfort zone. By embracing challenges, you can gain new knowledge and experience and develop new critical thinking skills. However, it's important to also recognize that failure is a natural part of the learning process. When you encounter setbacks or challenges, take the time to reflect on what went wrong and what you can do differently in the future.

It's also important to seek out feedback from others, whether it's from a mentor, colleague, or friend. Feedback can help you identify blind spots in your thinking and provide valuable insights for improvement.

Cultivating curiosity and a desire for knowledge

Cultivating curiosity and a desire for knowledge is another essential aspect of developing strong critical thinking skills. Stay up to date with the latest financial trends, learn new financial analysis techniques, and seek out new opportunities for growth and development.

One way to cultivate curiosity is to read widely and diversely. Don't limit yourself to just one subject or genre - explore a variety of topics and perspectives. You can also attend conferences, webinars, or workshops to learn from experts in your field.

Finally, don't be afraid to ask questions. Curiosity often starts with a simple question, and asking questions can help you gain a deeper understanding of a topic or issue.

Enhancing Your Analytical and Problem-Solving Skills

Strong analytical and problem-solving skills are essential for effective critical thinking in finance. By enhancing these skills, you can make sound financial decisions and drive growth and success for your organization.

One way to enhance your analytical and problem-solving skills is to practice breaking down complex financial problems. When faced with a complex financial problem, it can be overwhelming to try to solve it all at once. By breaking it down into smaller, more manageable components, you can analyze each component individually and consider its potential impact on the larger problem. This approach allows you to develop a more comprehensive understanding of the issue and identify potential solutions.

Another effective tool for enhancing your analytical and problem-solving skills is to utilize financial models and simulations. These tools can help you gain insights into potential financial outcomes, identify potential risks, and evaluate different financial strategies. By using financial models and simulations, you can test different scenarios and make more informed decisions about the best course of action.

In addition to financial models and simulations, leveraging data-driven insights can also be a powerful tool for enhancing your analytical and problem-solving skills. By analyzing financial data, identifying trends, and anticipating potential risks, you can develop sound financial strategies that promote financial success for your organization. Data-driven insights can help you make more informed decisions and avoid potential pitfalls.

Breaking down complex financial problems

Breaking down complex financial problems can be a daunting task, but it is an essential skill for effective critical thinking in finance. When faced with a complex financial problem, it can be helpful to start by identifying the key components of the problem. This might involve analyzing financial statements, reviewing contracts, or conducting research on industry trends.

Once you have identified the key components of the problem, you can begin to analyze each component individually. This might involve calculating financial ratios, conducting a SWOT analysis, or evaluating the potential impact of different scenarios. By breaking down the problem into smaller components, you can develop a more comprehensive understanding of the issue and identify potential solutions.

Utilizing financial models and simulations

Financial models and simulations are powerful tools for enhancing your analytical and problem-solving skills. These tools allow you to test different scenarios and evaluate the potential outcomes of different financial strategies. By using financial models and simulations, you can gain insights into potential risks and identify opportunities for growth.

There are many different types of financial models and simulations, including cash flow models, Monte Carlo simulations, and decision trees. Each of these tools has its own strengths and weaknesses, and it is important to choose the right tool for the job. By using financial models and simulations effectively, you can make more informed decisions and drive growth and success for your organization.

Leveraging data-driven insights

Data-driven insights are an increasingly important tool for enhancing your analytical and problem-solving skills. By analyzing financial data, identifying trends, and anticipating potential risks, you can develop sound financial strategies that promote financial success for your organization.

There are many different sources of financial data, including financial statements, market research reports, and industry benchmarks. By analyzing this data, you can identify patterns and trends that can help you make more informed decisions. For example, you might identify a trend of declining sales in a particular product line, which could prompt you to develop a new marketing strategy or explore new product offerings.

In addition to analyzing financial data, it is important to anticipate potential risks and challenges. This might involve conducting a SWOT analysis, evaluating the competitive landscape, or assessing the impact of regulatory changes. By anticipating potential risks, you can develop contingency plans and make more informed decisions.

Building Strong Communication and Collaboration Skills

Effective communication and collaboration are key components of success in the modern business world. In order to achieve financial success, it is important for individuals and teams to build and cultivate these skills. By doing so, you can more effectively share financial insights, coordinate financial activities, and drive growth and success for your organization.

Effectively presenting financial data and insights

One of the most important aspects of effective communication is presenting financial data and insights in a way that is clear, concise, and easy to understand. Utilizing visual aids, such as graphs and charts, can be a great way to make financial information more accessible and engaging. It is also important to tailor your communication style to your audience, whether it's senior leaders or front-line employees. By doing so, you can ensure that your message is received and understood by all.

Another important aspect of effective communication is being able to explain financial data and insights in a way that is relevant to your audience. For example, if you are presenting financial data to a marketing team, you may want to focus on metrics that are relevant to their work, such as customer acquisition costs or return on investment for advertising campaigns.

Encouraging open dialogue and diverse perspectives

Collaboration is all about encouraging open dialogue and diverse perspectives. By creating an environment where individuals feel comfortable sharing their thoughts and ideas, you can foster a culture of collaboration and innovation. It is important to be open to feedback from your colleagues and to encourage them to share their thoughts and ideas. Engaging in active listening is also key to understanding and appreciating different perspectives.

Another way to encourage collaboration is to create cross-functional teams that bring together individuals with different backgrounds and areas of expertise. By doing so, you can leverage the strengths and knowledge of each team member to drive success for your organization.

Fostering a culture of critical thinking within your team

Finally, fostering a culture of critical thinking within your team is essential for achieving financial success. Encouraging your team members to develop their critical thinking skills can help them make better decisions and solve problems more effectively. Providing opportunities for growth and development, such as training programs or mentorship, can also help your team members build their skills and increase their value to the organization.

Recognizing and celebrating the achievements of your team members is also important for fostering a culture of critical thinking. By acknowledging and rewarding individuals who demonstrate exceptional critical thinking skills, you can encourage others to follow their lead.

In conclusion, building strong communication and collaboration skills is essential for achieving financial success in the modern business world. By effectively presenting financial data and insights, encouraging open dialogue and diverse perspectives, and fostering a culture of critical thinking within your team, you can help your organization drive growth and success.

Improving your critical thinking skills as a VP of Finance is essential for driving financial success and growth for your organization. By understanding the importance of critical thinking in finance, assessing your current critical thinking abilities, developing a growth mindset, enhancing your analytical and problem-solving skills, and building strong communication and collaboration skills, you can become a more effective leader in the world of finance.

Ready to build an advisory board?

- Q1: Why are critical thinking skills important for a VP of Finance? A1: Critical thinking skills are essential for a VP of Finance as they help in analyzing information objectively, evaluating different perspectives, and making informed decisions to ensure financial stability and drive growth.

- Q2: What is the role of critical thinking in financial decision-making? A2: Critical thinking helps in evaluating different options and assessing their potential impacts on an organization. It helps to make informed choices and promote financial success.

- Q3: How can critical thinking skills enhance financial strategies? A3: Critical thinking helps in analyzing financial data, identifying trends, and anticipating potential risks, which help in developing effective financial strategies that promote long-term financial stability and growth.

- Q4: How can one assess their current critical thinking abilities? A4: One can assess their critical thinking abilities by evaluating their problem-solving skills, analyzing information, and seeking feedback from colleagues and mentors.

- Q5: How can one improve their communication and collaboration skills? A5: One can improve their communication and collaboration skills by presenting financial data and insights effectively, encouraging open dialogue and diverse perspectives, and fostering a culture of critical thinking within their team. It also involves creating an environment where individuals feel comfortable sharing their thoughts and ideas.

Build your advisory board today

See how easy we've made it to build an advisory board

See what boards you're qualified for

See what you qualify for with our 2-minute assessment

Similar Articles

How to Improve Your Decision Making Skills as a Chief Financial Officer

How to Improve Your Conflict Resolution Skills as a General Counsel

How to Improve Your Communication Skills as a VP of Security

How to Improve Your Networking Skills as a Chief Customer Officer

How to Improve Your Analytical Skills as a Chief Strategy Officer

How to Improve Your Time Management Skills as a Chief Executive Officer

How to Improve Your Time Management Skills as a Chief Sustainability Officer

How to Improve Your Teamwork Skills as a VP of Human Resources

How to Improve Your Emotional Intelligence Skills as a Chief Sales Officer

How to Improve Your Teamwork Skills as a Chief Operating Officer

How to Improve Your Time Management Skills as a VP of Administration

How to Improve Your Communication Skills as a Chief Human Resources Officer

How to Improve Your Presentation Skills as a VP of Administration

How to Improve Your Technical Skills as a Chief Procurement Officer

How to Improve Your Problem-Solving Skills as a VP of Operations

Start an advisory board.

Join an advisory board

- Affiliate Programs

- Affiliate Training

- Affiliates Reviews

- Cryptocurrency

The Art Of Critical Financial Thinking: Making Smarter Investment Decisions

Table of Contents

In “The Art Of Critical Financial Thinking: Making Smarter Investment Decisions,” you will discover the key principles and strategies necessary to navigate the complex world of investments with confidence and intelligence. By cultivating a critical mindset, you will learn to analyze market trends, assess risks, and identify profitable opportunities. This article explores how Capitalist Exploits Insider , a leading investment advisory service, can assist investors in developing their critical financial thinking skills to make informed and successful investment choices. Whether you are a seasoned investor or just starting out, this article offers valuable insights into maximizing your investment potential.

Understanding the Importance of Critical Financial Thinking

When it comes to making investment decisions, having a comprehensive understanding of financial concepts and factors is crucial. Critical financial thinking is a skill that enables investors to assess the complex financial landscape from multiple perspectives, helping them navigate uncertainties and make smarter choices. By developing a 360-degree view of the financial landscape, recognizing the impact of cognitive biases on decision-making, and evaluating the long-term implications of investment decisions, investors can enhance their financial decision-making process.

Developing a 360-degree view of the financial landscape

To make informed investment decisions, it is essential to have a holistic understanding of the financial landscape. This means considering various factors such as economic indicators, market trends, industry analysis, and company financial statements. By examining these different elements, investors can gain insights into the health of the economy, identify emerging trends, and evaluate the performance of specific companies.

Recognizing the impact of cognitive biases on decision-making

Human beings are prone to cognitive biases, which can cloud judgment and hinder rational decision-making. Understanding these biases and actively working to overcome them is crucial for critical financial thinking. By being aware of biases such as confirmation bias, overconfidence, and loss aversion, investors can strive to make objective and impartial decisions.

Evaluating the long-term implications of investment decisions

Investment decisions should not be based solely on short-term gains or losses. Critical financial thinking involves considering the long-term implications of an investment and the potential risks it may entail. By assessing factors such as industry trends, competitive landscape, and market conditions, investors can better determine the long-term viability and profitability of an investment opportunity.

Analyzing the Fundamentals: Key Factors to Consider

Before making any investment, it is vital to analyze the fundamentals of the investment opportunity. This involves a thorough assessment of company financial statements, an examination of industry trends and competitive landscape, and an analysis of macroeconomic indicators and market conditions.

Assessing company financial statements

Understanding a company’s financial statements is essential for evaluating its financial health and potential for growth. Key factors to consider include revenue growth, profitability, debt levels, cash flow, and liquidity. By analyzing financial statements, investors can gain insights into the company’s financial stability and its ability to generate sustainable returns.

Examining industry trends and competitive landscape

The performance of a company is influenced by the industry it operates in and the competition it faces. By examining industry trends, investors can identify growth sectors and potential opportunities. Additionally, analyzing the competitive landscape helps investors understand the company’s position in the market and its ability to stay ahead of competitors.

Analyzing macroeconomic indicators and market conditions

Macroeconomic indicators, such as GDP growth, interest rates, inflation, and employment rates, provide valuable insights into the overall economic environment. Understanding these indicators helps investors gauge the direction of the economy and anticipate potential market trends. By aligning investment decisions with prevailing market conditions, investors can improve their chances of success.

Identifying Investment Opportunities: Strategies and Techniques

Once investors have analyzed the fundamentals, it is essential to identify investment opportunities that align with their financial goals and risk appetite. Different investment strategies and techniques can be employed, including value investing, growth investing, contrarian investing, and trend following.

Value investing: Finding undervalued assets with potential

Value investing involves identifying assets that are trading below their intrinsic value. By conducting a thorough analysis of a company’s financials, investors can identify undervalued stocks or assets. The strategy is based on the belief that the market may not accurately reflect the true value of an asset, presenting an opportunity for investors to benefit from potential price appreciation.

Growth investing: Identifying companies with high growth potential

Growth investing focuses on identifying companies that have the potential for substantial growth in the future. Investors look for companies with high revenue growth rates, strong competitive advantages, and innovative business models. This strategy involves investing in companies at a relatively higher valuation in the hope that their growth prospects will justify the investment over time.

Contrarian investing: Taking advantage of market pessimism

Contrarian investing involves going against the prevailing market sentiment and investing in assets that are currently out of favor. The idea behind this strategy is that market sentiment can often be overly pessimistic, resulting in underpriced assets. By identifying assets that are undervalued due to market pessimism, investors can potentially profit from their eventual recovery.

Trend following: Riding the momentum of market trends

Trend following involves identifying and investing in assets that are experiencing sustained upward or downward price trends. This strategy relies on the belief that prices tend to continue in the same direction for a certain period of time. By following trends, investors aim to capitalize on the momentum of the market and profit from price movements.

Risk Management: Mitigating Potential Downsides

While investment opportunities present potential returns, they also come with risks. Effective risk management is an essential aspect of critical financial thinking. By implementing risk management strategies such as diversification, setting and reviewing investment objectives, using stop-loss orders, and stress testing investment portfolios, investors can mitigate potential downsides and protect their capital.

Diversification: Spreading risk across different asset classes

Diversification involves spreading investments across various asset classes, industries, and geographic regions. By diversifying their portfolio, investors reduce the impact of any single investment’s poor performance on their overall portfolio. This strategy helps mitigate risk and potentially improves the risk-return profile of the investment portfolio.

Setting and reviewing investment objectives

Before investing, it is crucial to establish clear investment objectives. Setting goals helps investors align their investment decisions with their desired outcomes. Regularly reviewing investment objectives allows investors to track their progress, make necessary adjustments, and ensure that their investments remain aligned with their goals.

Using stop-loss orders and risk-reward analysis

Stop-loss orders are instructions given to brokers or trading platforms to automatically sell a security if its price reaches a predetermined level. By utilizing stop-loss orders, investors can limit potential losses and protect their capital. Additionally, conducting risk-reward analysis helps investors assess the potential gains versus potential losses of an investment, allowing for informed decision-making.

Stress testing investment portfolios

Stress testing involves simulating various scenarios to assess the robustness of an investment portfolio. By subjecting the portfolio to hypothetical market conditions and economic shocks, investors can evaluate its performance under adverse circumstances. Stress testing helps identify potential weaknesses in the portfolio and informs adjustments to enhance its resilience.

Behavioral Finance: Understanding Investor Psychology

Investor psychology plays a significant role in financial decision-making. Emotions, cognitive biases, and social and herd behavior can all influence investment choices. Developing an understanding of behavioral finance allows investors to better manage their emotions, identify and overcome cognitive biases, and recognize the impact of social and herd behavior on investment decisions.

The role of emotions in investment decisions

Emotions such as fear, greed, and excitement can significantly impact investment decisions. It is essential for investors to be aware of their emotions and strive to make rational decisions based on solid analysis and research. Emotion-driven investment decisions can lead to impulsive actions that may not align with long-term investment objectives.

Overcoming cognitive biases and heuristics

Cognitive biases and heuristics are mental shortcuts that can lead to biased decision-making. Examples include confirmation bias, where investors seek information that confirms their existing beliefs, and availability bias, where investors rely on readily available information rather than conducting thorough analysis. By recognizing these biases and actively working to overcome them, investors can enhance their critical financial thinking skills.

Managing fear and greed in market fluctuations

Market fluctuations can trigger feelings of fear and greed among investors. During periods of market volatility, fear can lead to panic selling, while greed can result in chasing speculative investments. Managing these emotions and maintaining a disciplined investment approach is crucial for long-term success. By making decisions based on rational analysis rather than emotional impulses, investors can navigate market fluctuations more effectively.

The impact of social and herd behavior on investment decisions

Social and herd behavior can significantly influence investment decisions. When many investors follow the same investment patterns without conducting their own analysis, it can result in market bubbles or crashes. By understanding the impact of social and herd behavior, investors can make more informed decisions and avoid being swayed by market sentiment alone.

Leveraging Technology and Data in Financial Analysis

The advancement of technology has revolutionized financial analysis and decision-making. By leveraging advanced analytics, data-driven insights, automation, algorithmic trading, and financial platforms, investors can gain a competitive edge in the market.

Utilizing advanced analytics and data-driven insights

Analyzing vast amounts of data manually can be time-consuming and overwhelming. Fortunately, advanced analytics and data-driven insights have made it possible to extract valuable information from data quickly. By utilizing these tools, investors can identify patterns, trends, and correlations that may not be apparent through traditional analysis methods.

Automation and algorithmic trading

Automation and algorithmic trading involve using computer programs to execute trades automatically based on predefined rules and algorithms. These technologies enable investors to react swiftly to market changes and execute trades with precision. By taking advantage of automation and algorithmic trading, investors can reduce human error, enhance efficiency, and potentially improve investment performance.

Using financial platforms and tools for decision-making

Financial platforms and tools have made it easier for investors to access and analyze financial data. These platforms provide real-time market information, portfolio tracking, and financial analysis tools. By using these platforms, investors can conveniently monitor their investments, conduct research, and make more informed decisions based on accurate and up-to-date information.

Building a Framework for Critical Financial Thinking

Developing a framework for critical financial thinking lays the foundation for making sound investment decisions. By setting realistic expectations, continuously learning and staying updated with market trends, creating a well-defined investment strategy and plan, and seeking advice from experts, investors can enhance their decision-making process.

Setting realistic expectations and avoiding overconfidence

Having unrealistic expectations can lead to poor investment decisions and disappointment. It is crucial for investors to set realistic goals and expectations based on the prevailing market conditions and their risk tolerance. Additionally, avoiding overconfidence is important as it can cloud judgment and lead to excessive risk-taking.

Continuous learning and staying updated with market trends

The financial landscape is dynamic, and market trends evolve rapidly. Continuous learning and staying updated with market trends are essential for investors to adapt to changing conditions. By staying informed through reading financial news, attending seminars, and engaging in discussions with industry experts, investors can enhance their critical financial thinking skills.

Creating a well-defined investment strategy and plan

Creating a well-defined investment strategy and plan is crucial for success in the financial markets. This involves setting clear goals, determining the appropriate asset allocation, and establishing criteria for selecting investments. By having a structured approach, investors can make consistent and informed investment decisions aligned with their financial objectives.

Seeking advice and insights from experts

Even the most experienced investors can benefit from seeking advice and insights from experts. Consulting financial advisors, attending investment conferences, and participating in online communities can provide valuable perspectives and guidance. By leveraging the expertise of professionals, investors can gain new insights and make more informed decisions.

Exploring the Role of Capitalist Exploits in Financial Thinking

Capitalist Exploits offers a unique approach to critical financial thinking, helping investors navigate the complexities of the financial landscape and identify lucrative investment opportunities. By combining data-driven analysis, expert insights, and a contrarian mindset, Capitalist Exploits empowers investors to make informed decisions.

Understanding the unique approach of Capitalist Exploits

Capitalist Exploits takes a contrarian approach to investing, looking for opportunities that are often overlooked by the mainstream market. By focusing on asymmetric risk-reward profiles, Capitalist Exploits aims to identify investments with high upside potential and limited downside risk. This unique approach sets it apart from conventional investment strategies.

How Capitalist Exploits leverages critical financial thinking

Capitalist Exploits leverages critical financial thinking by conducting in-depth analysis of the financial landscape, including fundamental analysis, market trends, and risk management techniques. By combining this analysis with a contrarian mindset, Capitalist Exploits identifies investment opportunities that have the potential for significant returns while minimizing downside risk.

Real-life examples of successful investments with Capitalist Exploits

Capitalist Exploits has a track record of successful investments across various sectors and asset classes. By employing critical financial thinking and leveraging their unique approach, Capitalist Exploits has identified opportunities that have resulted in substantial returns for their investors. These real-life examples demonstrate the effectiveness of their strategies and techniques.

Unlocking the potential of critical financial thinking with Capitalist Exploits

Investors who explore critical financial thinking with Capitalist Exploits can unlock the potential for superior investment outcomes. By gaining access to expert analysis, contrarian insights, and proven investment strategies, investors can enhance their decision-making process and potentially achieve above-average returns. Capitalist Exploits provides a platform for investors to harness the power of critical financial thinking.

The Future of Financial Thinking: Emerging Trends and Opportunities

The financial landscape is constantly evolving, and staying ahead of emerging trends and opportunities is crucial for investors. By adapting to rapidly changing technologies and markets, exploring sustainable and ethical investing, seeking opportunities in emerging markets and sectors, and recognizing the evolving role of artificial intelligence, investors can position themselves for future success.

Adapting to rapidly changing technologies and markets

Technological advancements such as artificial intelligence, blockchain, and big data analytics are transforming the financial industry. Investors who adapt to these changes can gain a competitive advantage in analyzing data, identifying investment opportunities, and executing trades more efficiently. Staying updated with emerging technologies and market trends is essential for future success.

The rise of sustainable and ethical investing

As environmental and social concerns gain prominence, sustainable and ethical investing is becoming increasingly important. Investors who align their portfolios with companies that prioritize sustainability and ethical practices can not only generate financial returns but also contribute to positive social and environmental outcomes. The rise of sustainable and ethical investing presents opportunities for investors to make a positive impact while achieving their financial goals.

Opportunities in emerging markets and sectors

Emerging markets and sectors offer exciting prospects for investors. As economies evolve and industries expand, investors can identify high-growth opportunities that may not be fully recognized by the mainstream market. By conducting thorough research and leveraging critical financial thinking, investors can tap into the potential of emerging markets and sectors.

The evolving role of artificial intelligence in financial decision-making

Artificial intelligence is revolutionizing the financial sector, enabling faster and more accurate analysis, prediction, and decision-making. Machine learning algorithms can analyze vast amounts of data in real-time, identify patterns, and generate insights that humans may overlook. As artificial intelligence continues to evolve, its role in financial decision-making will become increasingly significant.

Conclusion: Mastering Critical Financial Thinking

Mastering critical financial thinking is an ongoing journey that requires continuous learning, adaptability, and the application of sound principles. By understanding the importance of critical financial thinking, analyzing the fundamentals, identifying investment opportunities, managing risks, understanding investor psychology, leveraging technology and data, building a framework, exploring the role of Capitalist Exploits, anticipating emerging trends, and applying critical financial thinking in real-world scenarios, investors can make smarter and more informed investment decisions. By mastering critical financial thinking, investors can navigate the complexities of the financial landscape and increase their chances of achieving their financial goals.

RELATED ARTICLES MORE FROM AUTHOR

Ai in marketing: the unseen game changer, my top 5 profit-leeching online business mistakes, the smart passive income brand and plans for the future, leave a reply cancel reply.

Save my name, email, and website in this browser for the next time I comment.

- FTC Full Disclosure

- Privacy Policy

- Our Mission

Resources and Downloads for Financial Literacy

Explore resources and downloads for educators seeking to help students learn financial concepts, practice money management, and build strong financial decision-making and economic-reasoning skills.

- What Is Financial Literacy? : Learn what it takes to become financially literate, why this set of knowledge and skills is so critical, and what this means for schools. (Edutopia, 2015)

- The Value of Financial Literacy : Take a look at this infographic for more information about what the research tell us about teaching finance to students. (Edutopia, 2012)

- Entrepreneurship Education Stresses Learning by Doing : Discover how entrepreneurship education can engage students’ critical thinking skills and deepen their financial literacy. You may also want to check out some of Edutopia’s resources and downloads related to entrepreneurship education . (Edutopia, 2011)

- Survey of the States : Explore takeaways of a biennial survey conducted by the Council for Economic Education that looks at the state of K–12 economic and financial education in the United States; an interactive companion to the survey dissects the costs of financial illiteracy and benefits and challenges of implementing financial and economic education. (Council for Economic Education)

- Why Teaching Financial Literacy Matters : Listen to a podcast from Vicki Davis’s Every Classroom Matters to learn why financial literacy is so important, and hear teacher Beth Werker describe a program called Enterprise City. (BAM Radio Network, 2014)

Discover Lessons, Simulations, Videos, and Apps

- 40-Plus Resources for National Financial Capability Month : Find resources for students of all ages in this compilation of games, lessons, hooks, apps, and more. (SmartBlog on Education, 2013)

- How to Promote Financial Literacy With Students : Discover video collections, online games, and structured curricula to help advance your teaching and learning goals. (KQED’s MindShift, 2013)

- Money as You Grow : Review 20 age-appropriate financial literacy lessons and activities for students in grades K-12. The companion website Money as You Learn includes tools for educators to integrate personal finance into teaching aligned with the Common Core State Standards.

- Online Economic Lessons : Browse or search a database with hundreds of free personal-finance lessons for grades K-12. (EconEdLink)

- National Standards in K–12 Personal Finance Education : View or download standards related to personal finance education across all grades K–12. (Jump$tart Coalition for Personal Finance Literacy)

- #FinEdChat and #FinancialLiteracy : Follow these hashtags on Twitter to keep up to date on the latest trends and resources for financial-literacy education.

Explore Activities for Grades K–8

- Creativity, Candy, and Commerce : Discover how middle school students brought curiosity and passion to learning through the design, manufacture, and marketing of their own signature chocolate bars. (Edutopia, 2015)

- Make the Money “Real” : Read about a counting-change simulation that gives students experience handling money in the lead-up to handling real transactions. (Edutopia, 2015)

- Teaching Toward an Affordable Future : Learn about a program that helps elementary school students learn about personal finance while saving money every week. (Edutopia, 2015)

- Elementary Financial Literacy: Lesson Ideas and Resources : Discover how financial literacy can be integrated into elementary English and mathematics, and find a few resources to get started. “ Financial Literacy for Elementary Students ” is another great list of resources. (Edutopia, 2014)

- Teaching Financial Literacy to Middle Schoolers : Explore strategies for integrating financial literacy into middle school curricula and age-appropriate resource suggestions. “ Financial Literacy for Middle School Students ” is another good source of guidance, information, and resources. (Edutopia, 2014)

Explore Activities for Grades 9–12

- Addressing Student, Family, and Community Needs : Find out how one school uses a personal finance class to impart lessons about fiscal responsibility and financial literacy to teens and connect this knowledge to their lives. (Edutopia, 2015)

- When Financial Education Hits Close to Home : Read about the Home Ownership project, a real-world project that helped students at Maplewood High School in Nashville, Tennessee, learn about homeownership and the power of personal finance. (Edutopia, 2015)

- 5-Minute Film Festival: We the Economy : Watch and share 20 short films that explain concepts like debt, money, and supply and demand. (Edutopia, 2015)

- Financial Literacy in High School: Necessary and Relevant : Learn how to make financial literacy relevant to students’ lives, and find resources for teaching financial literacy skills to high school students. For more guidance, information, and resources, also see “ Financial Literacy for High School Students. ” (Edutopia, 2014)

- 3 Ways to Enagage High Schoolers in Personal Finance : Discover a few technology-based ways to engage high schoolers in discussions about personal finance. (U.S. News and World Report, 2014)

- A Mobile App Lesson on Financial Capability : Check out a lesson on financial capability that makes use of mobile apps, courtesy of Brian Page, a high school personal finance and AP economics teacher. (Edutopia, 2013)

- Games to Teach Financial Literacy : Explore some friendly, engaging options to promote financial literacy among secondary students. (Edutopia, 2013)

Downloads and Examples From Schools That Work

Edutopia's flagship series highlights practices and case studies from K–12 schools and districts that are improving the way students learn. Below, find downloads used by practitioners at featured schools, and dive into real-world examples of teaching and learning financial literacy.

Piggy-Bank Friday: Life Skills Through Financial Literacy : Through the Piggy-Bank Friday program, K–5 students at Walter Bracken STEAM Academy in Las Vegas, Nevada, have saved over $30,000 in one year. Watch the video, read about their practice, and take a look at this featured download:

- School "Piggy-Bank" Deposit Slip : Print out these example deposit slips for your school's Piggy-Bank program.

Financial Literacy Makes School Relevant : The Ariel Community Academy, a public K–8 school on the South Side of Chicago, has been achieving remarkable success thanks to a number of effective strategies, particularly a financial-literacy program. Watch a video , and learn about the components of their K–8 curriculum to see how they do it. Then explore some of this school’s resources and downloads ; a few highlights from their Goods and Services Unit , organized according to Bloom’s Taxonomy , are linked below.

- Remembering : Review a lesson suggested for fourth grade that asks students to define and give examples of goods as objects that satisfy people's wants and services.

- Understanding : Review a lesson suggested for fifth grade that asks students to explain that economic wants are desires that can be satisfied by consuming a good or service or leisure activity and why not all wants can be satisfied.

- Applying : Review a lesson suggested for sixth grade that asks students to diagram the relationship among a final good or service, the way it’s produced, and who consumes and produces it.

- Analyzing : Review a lesson suggested for seventh grade that asks students to compare different ways resources are used to buy and consume goods and services.

- Creating : Review a lesson suggested for eighth grade that asks students to explain scarcity and how not all wants for goods and services can be satisfied.

Financial Analyst Skills

Learn about the skills that will be most essential for Financial Analysts in 2024.

Getting Started as a Financial Analyst

- What is a Financial Analyst

- How To Become

- Certifications

- Tools & Software

- LinkedIn Guide

- Interview Questions

- Work-Life Balance

- Professional Goals

- Resume Examples

- Cover Letter Examples

What Skills Does a Financial Analyst Need?

Find the important skills for any job.

Types of Skills for Financial Analysts

- Quantitative Analysis

Financial Reporting and Compliance

Strategic business understanding, communication and presentation skills, risk management and critical thinking, top hard skills for financial analysts.

Equipping analysts with robust quantitative, modeling, and data visualization skills to drive financial strategy and market insights.

- Advanced Excel and Spreadsheet Proficiency

- Financial Modeling and Valuation

- Data Analysis and Statistical Software

- Budgeting and Forecasting

- Accounting Principles and Financial Reporting Standards

- Risk Management Techniques

- Investment Analysis and Portfolio Management

- Knowledge of Financial Markets and Products

- Business Intelligence and Data Visualization Tools

Top Soft Skills for Financial Analysts

Empowering financial strategies through critical thinking, client rapport, and a keen eye for detail in dynamic market conditions.

- Effective Communication

- Problem-Solving and Critical Thinking

- Attention to Detail

- Adaptability and Flexibility

- Interpersonal Skills and Teamwork

- Time Management and Prioritization

- Leadership and Influence

- Emotional Intelligence

- Client Relationship Management

- Continuous Learning and Development

Most Important Financial Analyst Skills in 2024

Advanced data analysis and modeling, technological proficiency, regulatory and compliance knowledge, strategic business acumen, effective communication and presentation skills, risk management expertise, collaboration and teamwork, continuous learning and adaptability.

Show the Right Skills in Every Application

Financial analyst skills by experience level, important skills for entry-level financial analysts, important skills for mid-level financial analysts, important skills for senior financial analysts, most underrated skills for financial analysts, 1. behavioral economics understanding, 2. cross-cultural competence, 3. regulatory acumen, how to demonstrate your skills as a financial analyst in 2024, how you can upskill as a financial analyst.

- Master Advanced Data Analysis Tools: Proficiency in data analysis software such as Python, R, or Tableau is essential. Take courses to deepen your understanding of these tools and how they can be applied to financial data.

- Stay Abreast of Financial Regulations: Financial regulations are ever-changing. Regularly update your knowledge through webinars, courses, and seminars to ensure compliance and informed analysis.

- Enhance Your Understanding of Financial Modeling: Financial modeling is a cornerstone skill. Engage in advanced training to build more sophisticated models that can predict market trends and inform investment decisions.

- Develop Blockchain and Cryptocurrency Acumen: With the rise of digital assets, understanding blockchain technology and cryptocurrency markets can give you an edge in modern financial analysis.

- Expand Your Knowledge in ESG Investing: Environmental, Social, and Governance (ESG) criteria are becoming increasingly important. Learn how to integrate ESG factors into investment analysis and decision-making.

- Improve Communication Skills: A Financial Analyst must convey complex information clearly. Work on your presentation and storytelling skills to effectively communicate your analyses to stakeholders.

- Build a Strong Professional Network: Connect with other finance professionals through networking events and online communities to exchange knowledge and stay informed about industry trends.